In This Article

Over the past decade, corporate financial reporting has shifted from static PDFs to intelligent, data-driven disclosures. Inline XBRL (iXBRL) sits at the heart of this transformation. It allows companies to file a single version of a report that humans can read and machines can analyze simultaneously. For CFOs and compliance teams, mastering iXBRL tagging is no longer an IT exercise; it’s a reporting necessity.

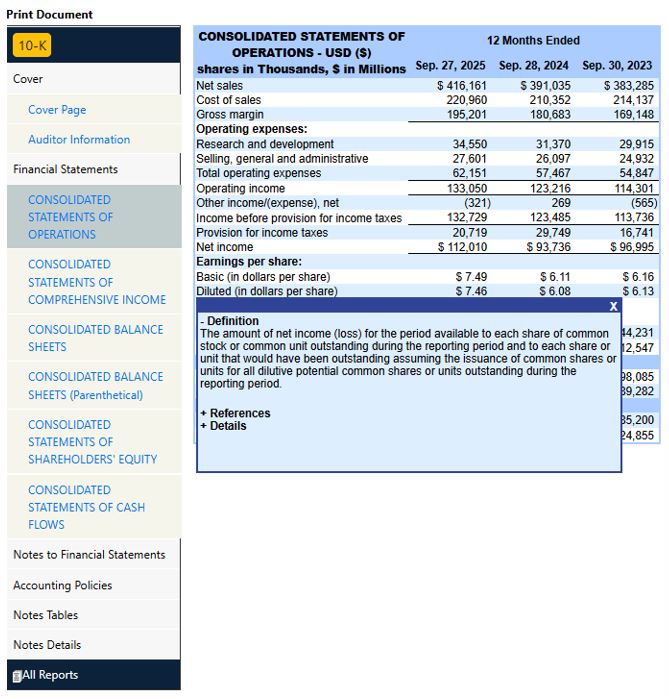

In practice, this format helps investors, regulators, and analysts extract and compare key financial information in seconds. A properly tagged balance sheet from a company like Apple Inc. can be analyzed alongside thousands of others, revealing performance trends without anyone touching a spreadsheet.

The SEC now mandates that all public companies file in iXBRL format under Regulation S-T. For foreign private issuers reporting under IFRS, the requirement follows the same principles. This guide explains how iXBRL tagging works in practice, which rules govern it, and what steps companies can take to avoid common errors and validation issues.

What is iXBRL? Understanding the Basics

Inline XBRL, or iXBRL, is the modern standard for submitting financial reports to regulators like the SEC. It combines human-readable HTML and machine-readable XBRL data in one seamless document. In other words, what investors see on screen is the same file that computers analyze, eliminating the need for separate exhibits or manual data extraction.

For example, when Microsoft Corporation files its quarterly Form 10-Q, the revenue figure that appears on page one of the HTML report is also encoded beneath the surface using an XBRL tag. This tag, such as us-gaap:Revenues, tells data systems exactly what that number represents and what accounting standard it follows.

Each iXBRL tag corresponds to a defined concept in a taxonomy, a structured list of financial elements maintained by the Financial Accounting Standards Board (FASB) for U.S. GAAP or by the IFRS Foundation for international filers. These taxonomies ensure consistency, allowing investors and analysts to compare similar data points across thousands of companies.

Unlike older filing formats, iXBRL does not require separate XBRL instance documents. Instead, the tagging is embedded directly into the filing, streamlining validation and review. The SEC’s adoption of this approach reflects a broader trend toward automation and data standardization across financial reporting.

Need Reliable EDGAR Filing Support?

Our responsive specialists manage SEC filings, newswire distribution, and print services for clients nationwide.

Key Components of iXBRL Tagging

Every iXBRL filing is built from a few essential components that define, structure, and validate the information reported. Understanding these elements helps filers maintain consistency and accuracy across reporting periods.

At its core, tagging translates the information presented in financial statements into structured data that aligns with accounting standards. Think of it as labeling each figure and description so that both humans and systems interpret it the same way.

Below is a summary of the key iXBRL components used in SEC filings:

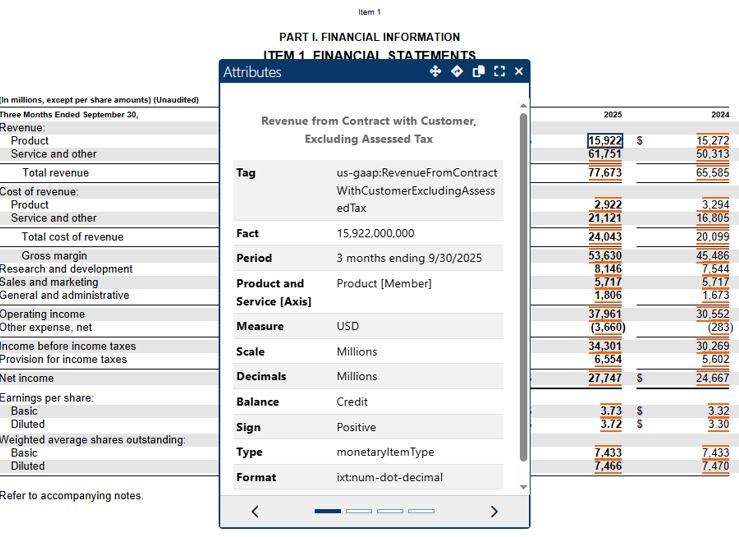

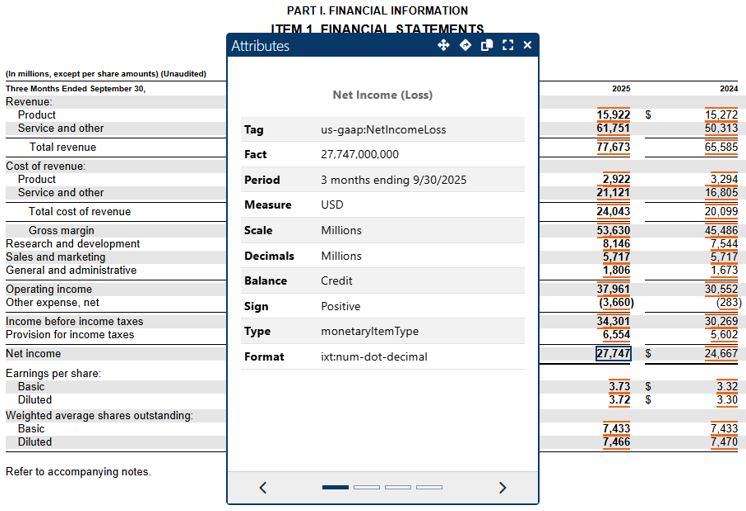

| Component | Purpose | Example |

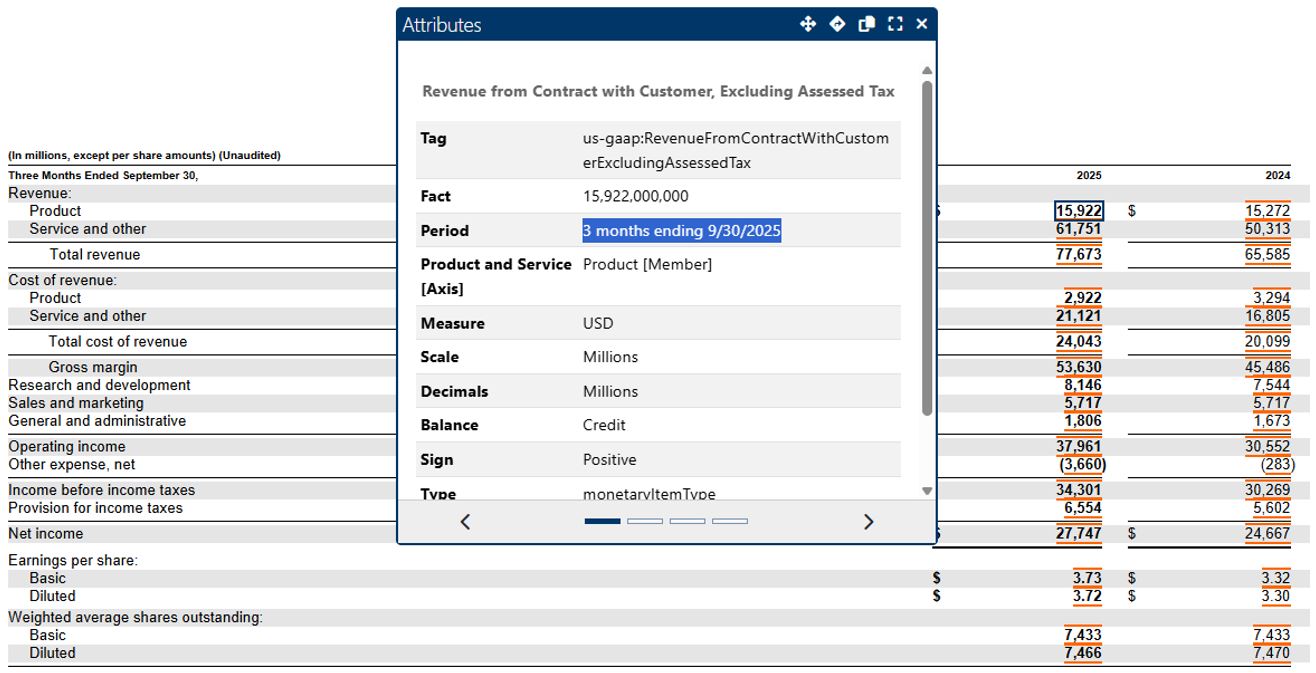

| Tag | Machine-readable identifier applied to each data point in a report. | “Revenues” tagged as ‘us-gaap:Revenues’ |

| Context | Defines the reporting entity and period for a tagged item. | FY2024, Consolidated Entity |

| Unit | Specifies the measurement standard for the data. | USD, Shares, Percentage |

| Taxonomy | The standardized dictionary of reporting elements used for tagging. | U.S. GAAP 2024 Taxonomy |

| Footnote / Reference | Provides additional explanations or clarifications linked to tags. | Narrative note on revenue recognition |

Context Example

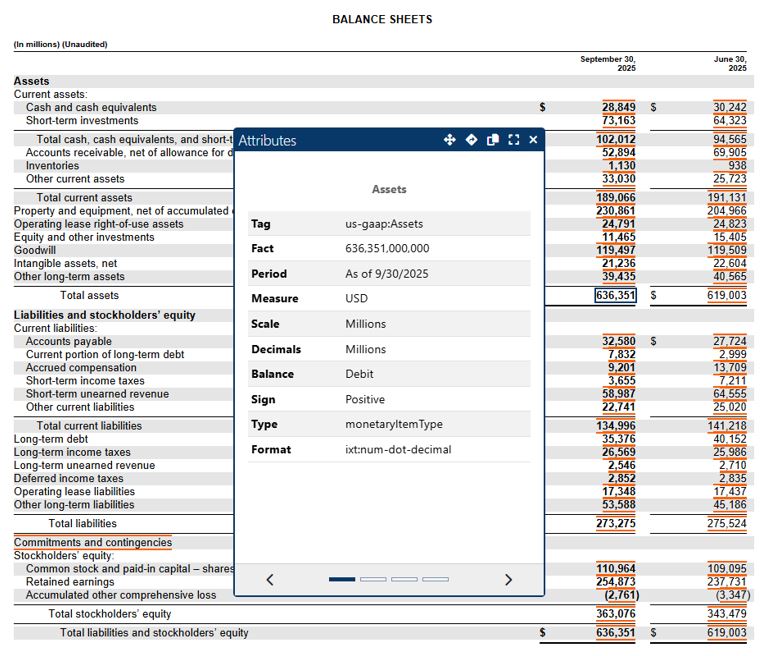

When Apple Inc. reports “Cash and Cash Equivalents” as of September 30, 2024, the context defines both the reporting entity and the time period, ensuring the tag applies specifically to Apple’s balance sheet for that fiscal quarter.

Unit Example

A unit defines the measurement applied to a data point. For instance, “Revenues” might be expressed in USD, while share counts use “shares.” Consistent use of units helps the SEC’s validation system and external data platforms interpret numeric values correctly.

Footnotes and Labels

Footnotes and labels give meaning to the tagged data. Labels describe what each tag represents, while footnotes provide additional clarification. For example, if Tesla, Inc. includes a one-time regulatory credit in “Automotive Revenue,” a footnote explains this detail without affecting the numerical tag itself.

Together, these components make the iXBRL format both flexible and standardized, flexible enough to reflect each company’s disclosures and standardized enough for automated comparison across all SEC filers.

How the iXBRL Tagging Process Works

Tagging a financial report in iXBRL follows a structured but flexible process that moves from document preparation to final SEC submission. While the technical steps may vary depending on the software used, the overall workflow remains consistent across all filers.

iXBRL process may feel like it’s a loop: prepare, tag, validate, review, and file. Each stage builds on the previous one, and skipping even a small detail can lead to validation errors or rejected filings.

1. Preparing the Source Document

The process begins with a finalized HTML version of the financial report. All figures, headings, and narrative disclosures should be complete before tagging starts. If any changes occur after tagging begins, it can create mismatches between labels and tags during validation.

2. Mapping Tags to Financial Concepts

Next, the tagging specialist maps each financial item to the appropriate element from the taxonomy. For example, when Amazon reports “Net Sales,” it must be linked to the correct XBRL concept (us-gaap:Revenues) rather than a similar but incorrect one like us-gaap:RevenuesNetOfInterestExpense.

This step requires a careful understanding of both the accounting meaning of the item and how it fits within the taxonomy’s structure. Mistagging an element can cause calculation discrepancies, leading to SEC comment letters or the need for amended filings.

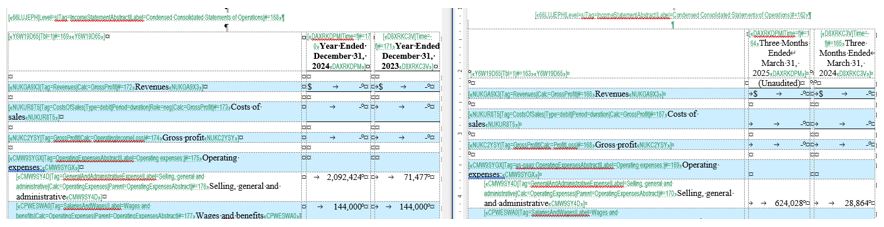

3. Applying Contexts, Dates, and Units

Each tagged figure must be associated with a specific context that includes the entity identifier, reporting period, and measurement unit. For instance, “Total Assets” as of December 31, 2024, uses a date context representing a single point in time, while “Revenue” covers a range of dates for the fiscal year.

Accurate context tagging ensures the SEC’s validation systems recognize whether the reported figures represent a balance at period-end or results over time.

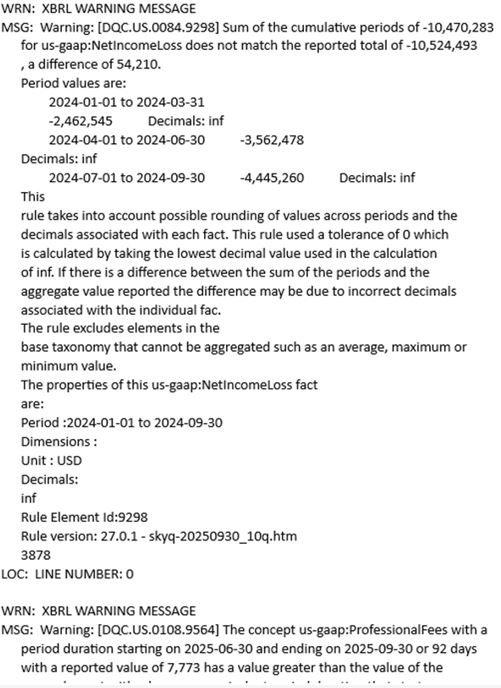

4. Reviewing and Validating the Tagged Report

Once all tags are applied, the next step is validation. The filer runs the iXBRL validation tool, either built into the software or through the SEC’s own viewer, to detect calculation errors, missing tags, or outdated taxonomy references.

This stage catches many common issues before submission. For example, if Microsoft uses a 2023 taxonomy element in a 2024 filing, the validation report will flag it for correction.

Example: In one Southridge project, a client’s income statement failed validation because “Earnings per Share” was tagged with an incorrect period context. A quick re-tag fixed the error and prevented an SEC rejection.

5. Generating the Inline Report and Submitting to EDGAR

After successful validation, the software exports a single HTML file containing all embedded tags. This iXBRL report is then submitted to EDGAR through the company’s account or via an authorized filing agent.

Once accepted, the filing becomes public on SEC.gov and can be viewed interactively by investors, analysts, and regulators. Most companies perform a final review in the SEC viewer to confirm that all values and tags display correctly.

6. Post-Filing Review

6. Post-Filing Review

After submission, it’s best practice to perform a brief post-filing audit to confirm that the data displayed on SEC.gov matches the internal financial statements. This step helps identify any discrepancies early, particularly if updates to the taxonomy or filing software occur mid-year.

By following this end-to-end tagging workflow, filers can minimize errors, streamline review time, and ensure that their financial disclosures remain both compliant and transparent. iXBRL tagging is not just about meeting a technical requirement; it’s about making financial data accessible, comparable, and credible in a digital-first regulatory environment.

Final Pre-Filing Checklist:

- Finalize numbers and confirm that all figures and narrative disclosures match the approved financial statements.

- Verify that every major statement and schedule (balance sheet, income statement, cash flows, and equity) has been tagged.

- Ensure all contexts, dates, and units are correctly defined for each tag.

- Validate the file in both your tagging software and the SEC’s Inline Viewer.

- Review labels and footnotes for clarity and consistency.

- Lock the final version before transmitting to EDGAR.

SEC Requirements for iXBRL Filings

The SEC mandates Inline XBRL (iXBRL) for nearly all public companies to enhance data accuracy, accessibility, and comparability across financial disclosures. What began as a pilot program in 2009 is now a core compliance requirement for periodic filings, registration statements, and mutual fund reports.

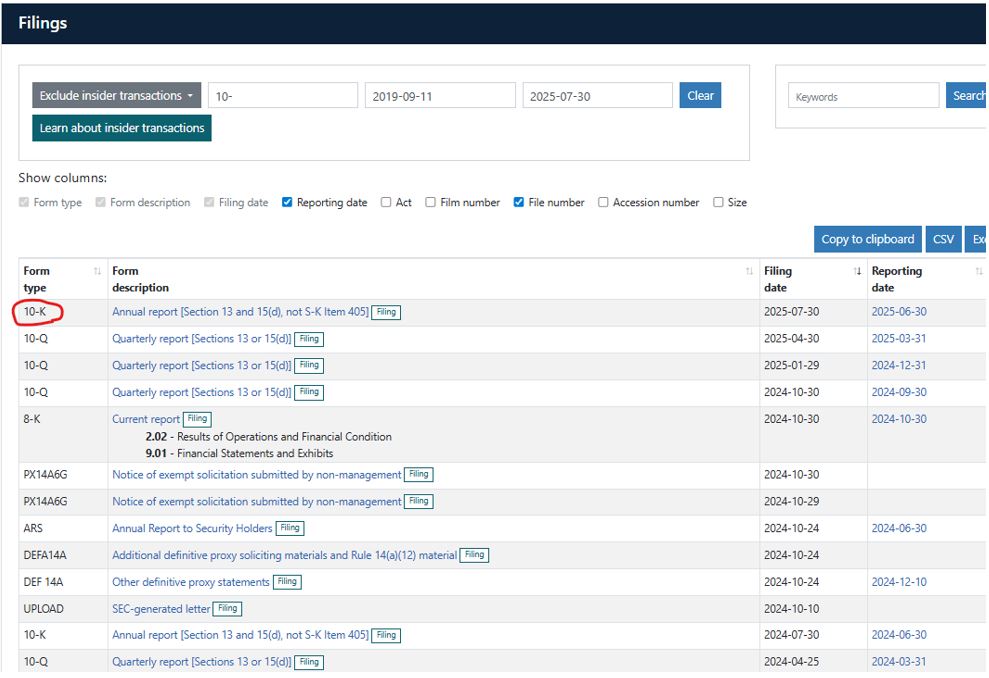

Which Filings Require iXBRL Tagging

All U.S. domestic filers submitting financial statements under U.S. GAAP are required to file their reports in iXBRL format. This includes periodic reports such as Form 10-K and Form 10-Q, Form 8-K, as well as registration statements like Forms S-1, S-3, and S-4. Foreign private issuers reporting under IFRS must also submit their financials using the IFRS taxonomy approved by the SEC.

Mutual funds and investment companies file iXBRL for their risk/return summaries (Form N-1A) and portfolio holdings (Form N-PORT), ensuring transparency in investment performance and risk data.

Tagging Requirements and Taxonomy Standards

Each iXBRL submission must use the latest version of the U.S. GAAP Financial Reporting Taxonomy or the IFRS Taxonomy, depending on the filer’s accounting basis. The taxonomy is updated annually to reflect new accounting standards, terminology changes, and improved element definitions.

Companies like Pfizer or Coca-Cola routinely update their tagging templates each year to stay aligned with the latest taxonomy release. Using outdated elements can trigger validation errors or create inconsistencies in reported data.

Cover Page Tagging (Exhibit 104)

In 2020, the SEC expanded tagging requirements to include cover page data from key filings such as the Form 8-K. Information such as the company name, ticker symbol, trading exchange, form type, and report period end date must be tagged in Inline XBRL and attached as Exhibit 104.

For example, the cover page of Microsoft’s Form 10-K must include tags identifying its trading symbol (MSFT) and the exchange (NASDAQ). These cover page tags improve searchability and ensure key filing details are machine-readable.

Validation and Submission Standards

All filings are validated through the SEC’s EDGAR system before acceptance. Validation checks for structural errors, calculation inconsistencies, missing tags, and schema mismatches. The SEC’s Inline XBRL Viewer enables filers to preview their documents exactly as investors will see them once published.

If a filing fails validation, it will be “suspended” in EDGAR until corrected and resubmitted. Common causes of suspension include missing context information, duplicate tag use, and misaligned calculation relationships.

Ongoing Compliance and Annual Updates

The SEC expects filers to maintain consistent tagging across periods. This means the same concept, like “Revenue” or “Operating Income”, should use the same XBRL element every quarter unless there is a valid accounting change.

Many large issuers, such as Apple or Procter & Gamble, maintain internal tagging libraries reviewed annually by accounting and compliance teams. Consistency not only reduces errors but also builds confidence with investors who rely on these datasets for trend analysis.

Common Challenges in iXBRL Tagging

Even experienced filers encounter challenges when preparing Inline XBRL reports. Tagging requires precision and judgment, and small inconsistencies can create major validation issues or lead to SEC comment letters. Many of these challenges stem from misapplied tags, outdated taxonomies, or gaps between accounting and compliance teams.

Selecting the Wrong Tag

One of the most frequent mistakes occurs when filers choose an element that looks correct but represents a different accounting meaning. For instance, if Microsoft tags “Revenue” using us-gaap:SalesRevenueNet when its disclosure includes both product and service revenue, it might need the broader us-gaap:Revenues tag instead. Such mismatches distort comparability and can trigger validation alerts.

Example: When a company reports “Operating Profit” but mistakenly tags it as “Net Income,” it affects every downstream analysis—from industry benchmarking to automated investor dashboards.

Using Outdated or Deprecated Taxonomies

The SEC updates its U.S. GAAP and IFRS taxonomies every year. Using a previous version can cause deprecated tags, meaning the system no longer recognizes them as valid. This can lead to “suspended” filings during validation.

Companies like Apple and Pfizer typically update their tagging templates at the start of each fiscal year to align with the latest taxonomy. Smaller issuers that skip this step often face rework late in the process.

Inconsistent Tagging Across Periods

Consistency is one of the most overlooked elements of high-quality iXBRL tagging. When the same financial concept is tagged differently across quarters or years, the SEC’s analytics systems may treat them as separate data points.

For example, if a company uses one tag for “Operating Expenses” in Q1 and a different tag in Q3, automated comparisons will break. Southridge often helps filers conduct tag consistency audits before submitting annual reports to ensure uniform tagging throughout the year.

Incorrect Contexts and Units

A frequent source of filing rejections comes from assigning the wrong date context or measurement unit. A balance sheet item like “Total Assets” should have an instant date (a single point in time), while “Revenue” should span a duration period.

Similarly, mixing up units, such as labeling figures in thousands when the taxonomy expects full dollars, can lead to misleading totals. Most tagging platforms flag these inconsistencies, but manual review remains essential.

Missing or Improperly Tagged Footnotes

Footnotes add essential narrative detail to tagged numbers. When companies fail to tag these notes or attach them to the wrong element, important explanations are lost to data consumers.

For instance, if Tesla reports “Other Income” that includes regulatory credits, but fails to tag the footnote explaining that breakdown, automated analysis tools will interpret the value as ordinary income. The SEC emphasizes complete footnote tagging to maintain context and transparency.

Calculation Linkbase Errors

Calculation relationships define how financial items add up, for example, how “Total Liabilities and Shareholders’ Equity” equals the sum of its components. If any item’s tag or context is inconsistent, the calculation fails validation.

Southridge often sees this when filers manually edit tagged totals or when rounding differences cause small mismatches. While the SEC allows minor variances, large discrepancies may lead to a rejected submission.

Over-Tagging and Redundant Elements

Some filers try to tag every number and text block, leading to redundancy and confusion. The SEC encourages filers to tag key disclosures and avoid duplicating information unnecessarily. Over-tagging increases validation time and makes reports harder to interpret.

A balanced approach, tagging all material financial items while leaving immaterial or repetitive data untagged, produces cleaner, more reliable filings.

Lack of Coordination Between Accounting and Compliance Teams

Tagging accuracy depends heavily on collaboration between finance, accounting, and compliance professionals. A common mistake occurs when teams work in silos; accountants understand the numbers, but the tagging team applies them without context.

We recommend maintaining a shared tagging checklist and conducting joint reviews before validation. This reduces miscommunication and ensures the tags reflect the true intent of the financial statements.

Compliance Standards and Best Practices

Compliance with Inline XBRL requirements is not just a matter of meeting deadlines; it’s about maintaining consistency, accuracy, and transparency across every report. The SEC’s iXBRL mandate aims to make financial data both machine-readable and investor-friendly, but achieving that balance requires disciplined processes and strong internal controls.

Follow Current Taxonomy Standards

Every iXBRL filing must use the latest taxonomy approved by the SEC or IFRS Foundation which is released and maintained by the FASB on its website. Outdated tags can lead to validation errors or create inconsistencies in trend analysis. For example, when Johnson & Johnson transitioned to the 2024 U.S. GAAP taxonomy, it replaced several deprecated elements related to “Research and Development Expense” and “Inventory Valuation.”

Maintain Consistent Tagging Across Periods

Consistency is one of the hallmarks of high-quality XBRL data. Investors and analysts rely on the same tags being used quarter after quarter for comparable concepts. A company that tags “Operating Income” differently in its 10-K and 10-Q filings creates noise in data analytics and may receive an SEC comment letter asking for clarification.

At Southridge, our team regularly performs cross-period tag consistency reviews, comparing a company’s filings across two fiscal years to confirm uniform tagging and labeling practices.

Validate Early and Validate Often

Validation is the most effective quality control step in the tagging process. Running an initial validation after mapping the major financial statements helps catch problems early—like duplicate contexts or incorrect label links.

For instance, Amazon’s compliance team performs at least three validation rounds for each quarterly filing: once after tag mapping, again before sign-off, and finally right before submission to EDGAR. This process ensures that no deprecated tags or rounding errors slip through.

Use Structured Workflows and Audit Trails

Modern iXBRL platforms like Workiva, GoXBRL, and DataTracks provide built-in workflows and user logs. These features track changes, tag updates, and user actions — essential for audit readiness and accountability.

Companies with large reporting teams benefit from assigning role-based access, where preparers, reviewers, and approvers each have distinct permissions. This minimizes accidental overwrites and ensures a proper review chain before submission.

Document Your Tagging Decisions

Keeping a centralized tagging reference sheet is one of the best defenses against inconsistency. Each time a new tag is introduced or changed, record the rationale and date. Over time, this creates a “tagging history” that helps explain past decisions to auditors, regulators, or new team members.

Example: If “Deferred Tax Asset” was reclassified to “Noncurrent,” note the change and the updated tag ID (us-gaap:DeferredTaxAssetsNoncurrent). Doing so ensures future reports continue the correct tagging pattern.

Perform Post-Filing Reviews

After submitting the iXBRL filing to EDGAR, companies should perform a post-filing validation directly in the SEC’s Inline XBRL Viewer. This confirms that every tag displays correctly and that hyperlinks, footnotes, and calculation relationships are intact.

Many issuers, including Procter & Gamble and Pfizer, maintain internal review checklists that must be completed within 24 hours of filing acceptance. These include verifying tag placement, formatting, and accessibility for screen readers.

Stay Aligned with Evolving SEC Guidance

The SEC continues to refine its guidance on iXBRL through regular updates to the EDGAR Filer Manual. New rules, such as cover page tagging and digital signature requirements, can affect how filings are structured.

Following these updates not only ensures compliance but also positions your filings for better machine readability and analytics compatibility. Southridge frequently monitors these updates and shares client advisories summarizing any rule changes that affect quarterly and annual reporting cycles.

Global Adoption of iXBRL and the Rise of International Digital Reporting Standards

The success of iXBRL in the United States has inspired a wave of similar initiatives worldwide, as regulators move toward greater transparency and standardization in corporate reporting. Today, structured digital reporting is no longer limited to SEC filers — it is becoming a global expectation.

Europe: The ESEF Framework

In the European Union, the European Single Electronic Format (ESEF) has made Inline XBRL mandatory for all listed companies since 2021. Supervised by the European Securities and Markets Authority (ESMA), this framework ensures that annual financial reports are both readable and machine-parseable.

Under ESEF, companies must tag their consolidated financial statements using the IFRS taxonomy, similar to how U.S. issuers use U.S. GAAP. Major European groups like Siemens AG and Unilever PLC now publish their annual reports in iXBRL format, enabling investors to compare disclosures seamlessly across markets.

United Kingdom and Asia-Pacific

The United Kingdom’s Financial Conduct Authority (FCA) adopted iXBRL for regulatory filings years earlier, setting the stage for more widespread digital reporting.

Across the Asia-Pacific, countries like Japan, Singapore, and South Korea have implemented their own structured data frameworks. Japan’s Financial Services Agency (JFSA) was among the earliest adopters, mandating XBRL submissions for listed firms through the EDINET system.

Singapore’s Accounting and Corporate Regulatory Authority (ACRA) uses XBRL for all corporate financial statements, while South Korea’s DART system integrates Inline XBRL to improve investor access and reporting consistency.

Emerging Markets and Global Convergence

Emerging markets are rapidly following suit, recognizing the advantages of structured reporting for both domestic oversight and international investment. Countries in the Middle East and Latin America are piloting XBRL-based disclosure systems to align with international reporting practices.

Organizations such as XBRL International and IFRS Foundation continue to work toward harmonizing taxonomy standards, reducing discrepancies between U.S. GAAP, IFRS, and regional frameworks. The long-term vision is clear — to make corporate financial data globally comparable and accessible in real time.

Key Takeaways

Inline XBRL has transformed how companies communicate their financial performance. It bridges the gap between human-readable reports and structured data, giving investors and regulators instant access to accurate, comparable information. What once required spreadsheets and manual review is now handled through automation and intelligent validation tools, provided that filers follow sound tagging and compliance practices.

The real value of iXBRL goes beyond meeting SEC requirements; it builds confidence. Investors gain clearer insights, analysts make better comparisons, and companies demonstrate accountability in a digital marketplace that values transparency more than ever.

If your organization is preparing for an upcoming filing or looking to refine its digital reporting process, explore how our iXBRL Filing Services can help streamline compliance and improve reporting accuracy.